Frothy Markets Spark Worries of Bubbles in European Assets

- Investors, analysts highlight pricing excesses across assets

- Stretched valuations follow central bank-fuelled rally

The almost uninterrupted rally in European stocks and corporate bonds over the past year has sent valuation metrics to frothy levels, setting the stage for potential pull-backs as Europe struggles with its vaccine rollout which could imperil the region’s economic recovery.

With Europe’s equity benchmark trading at a near record-high valuation level, the word “bubble” is creeping into analysts’ notes, following sharp gains fueled by unprecedented stimulus measures from central banks and governments fighting the economic impact from the pandemic.

While returns-hungry investors continue to pile into risky assets, a number of strategists warn of a growing disconnect between prices and the economic reality in various corners of the market, from Europe’s renewable energy shares to investment-grade corporate bonds.

“Compartments of the markets have moved significantly above fair value,” said Kasper Elmgreen, head of equities at Amundi. “Gravity is a powerful force, where there are bubbles building they will eventually burst no matter how elevated valuations can become before this happens.”

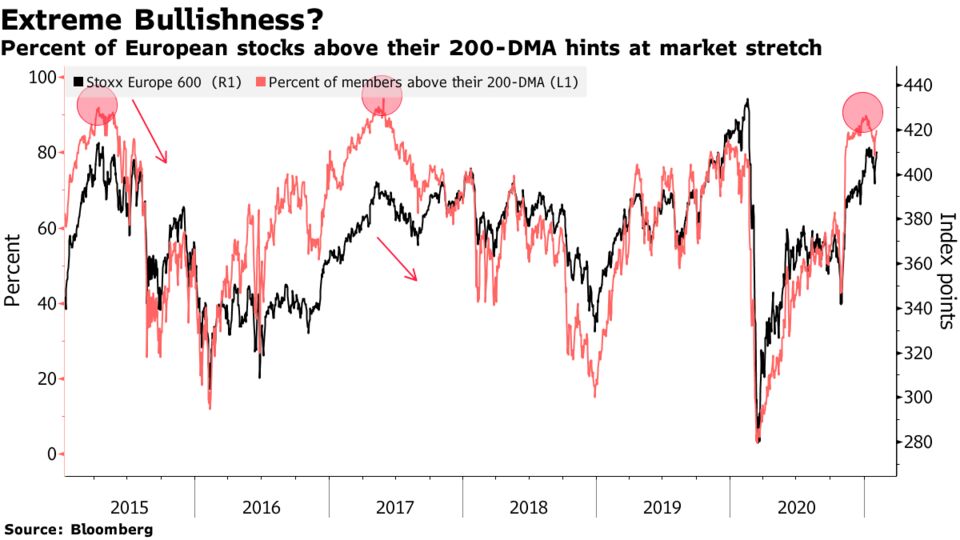

The Stoxx Europe 600 Index -- which just recorded its best weekly gain since mid-November, up 3.5% -- trades at 17 times forward earnings, well above its 10-year average of around 14 times. In early January, about 90% of Stoxx 600 were trading above their 200-day moving average, the most since 2017, near a level that turned out to be a technical sell signal in the past.

The markets got their latest boost after day-traders triggered a boom, followed by rapid declines, in shares of companies like Gamestop Corp. and Nokia Oyj as short sellers rushed to unwind negative bets. While the brawl between the retail traders and hedge funds has abated, it is seen by many analysts and investors as a sign the market is overheating.

“Increased retail participation in equity markets is a typical side effect of bull markets and of bull markets overshooting into bubbles,” said Lars Kreckel, global equity strategist at Legal & General Investment Management.

Another worrying trend is the outperformance since October of European companies with weaker balance sheets. That phenomenon, like the day-trader drama, is a function of cheap money that’s emboldening investors to take risks, and is “symptomatic of a very frothy and speculative market,” said Suzanne Hutchins, a portfolio manager at Newton Investment Management.

“Markets are fragile and the manipulation by central banks keeping a tight lid on interest rates creates lots of unforeseen risks,” she said.

While European stocks are still nowhere near record valuation levels seen on Wall Street, one segment has seen astronomical surges: renewables. Even after the recent retreat, Indxx Renewable Energy Index is trading at 40 times earnings, double the multiple of the MSCI World Index.

Bank of America Corp. strategists said clean-energy ETF flows are creating potential bubbles in stocks like EDP Renovaveis SA, Orsted AS and Verbund AG. The fourth-quarter rally of more than 40% in these European utilities coincided with a fourfold increase in flows to the iShares Global Clean Energy ETF.

On measures such as momentum, valuations and multiples against growth expectations, clean-energy shares “are certainly not cheap and in many cases look quite stretched,” said Stuart Joyner, an analyst at Redburn.

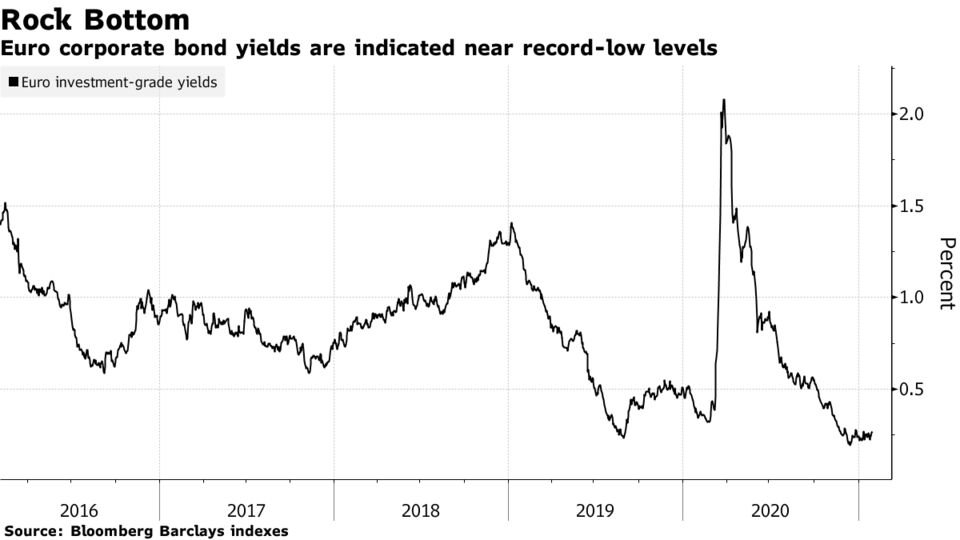

Similar concerns have been brewing over the rich prices of high-grade corporate bonds. The rally in the credit market, which began last March, thanks to central bank support, has stalled in Europe. Investors see little reason to bid up company debt, and analysts are urging them to refrain from further purchases until prices drop.

“A peak seems to have been reached,” said Sebastien Barthelemi, head of credit research at Kepler Cheuvreux SA.

High-grade euro corporate bonds are yielding about 0.3%, and junk-rated euro bonds have followed a similar path this year, driving asset managers toward riskier assets like equities in their hunt for returns.

“People who used to invest only in investment-grade will not be able to live with yields they are getting,” said Jeremy Ghose, head of the credit management business at Investcorp. “You are really getting peanuts today.”

Still, for all the talk of expensive valuations, a collapse in corporate bond prices has yet to materialize as credit portfolio managers keep deploying cash and the European Central Bank buys debt under its QE programs. “It looks strange to see all this frenzy in new issues but the search of yield prevails for investors,” said Barthelemi.

This has allowed the return of risky deals in the junk-rated market, such as payment-in-kind notes, bonds deep in junk territory and companies issuing debt just to fund dividends.

And in the equity market, the recent run-up in equities could be “pre-pricing of the extremely strong growth conditions that are likely to materialize this year,” according to Sebastian Raedler, a strategist at Bank of America.

Nevertheless, cases like Gamestop are bound to raise questions about the health of the broader market.

“Concerns are mounting as to whether financial markets may have entered bubble territory over the past few weeks,” Frederique Carrier, head of investment strategy at RBC Wealth Management, wrote in a note. “Instances of excessive behavior in markets have become apparent, and, it seems, more frequent.”

No comments:

Post a Comment