SHULI REN, A COMPLETE AND UTTER CHINESE RAT BASTARD, IS A DASTARDLY BEIJING ACOLYTE. WHATEVER MOVED HIM TO WRITE THIS TRUTHFUL PIECE? A LIGHTENING BOLT FROM A DIVINITY?

Cash Flow Analysis Is a Losing Game in China

Americans should count themselves lucky. Transparency makes investing in distressed companies much less hazardous than in the People’s Republic.

Investing in distressed companies is never easy but can reap huge rewards. Last month, amid the retail trading frenzy sparked by GameStop Corp., Jason Mudrick’s $3.1 billion hedge fund made almost $200 million, the bulk of which came from debt and equity options of AMC Entertainment Holdings Inc.

However, cash flow analysis and other research won’t get you anywhere with distressed companies in China, which can trip up even the most diligent treasure hunter. There, you’ve got to have an in; access to company information is everything.

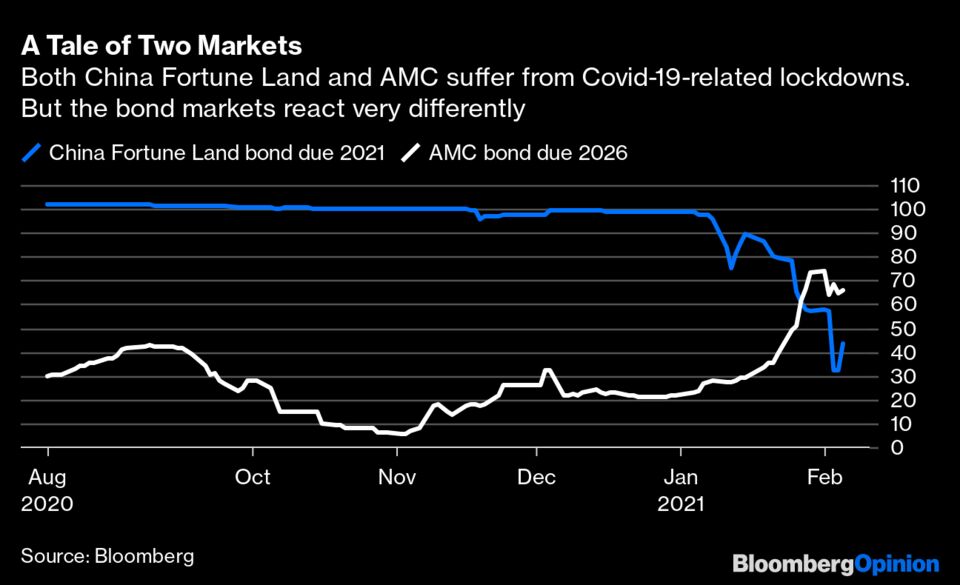

Take China Fortune Land Development Co., the country’s largest industrial park developer. The company spun into trouble in January when resurgent Covid-19 cases prompted China to lock down parts of Beijing and neighboring Hebei province, where the developer generated 55% of its revenue in 2019.

Since then, investors have been spending sleepless nights following the drama. China Fortune Land is a big debt issuer, with $4.6 billion dollar bonds outstanding alone. If it fails to repay a $530 million issue due Feb. 28, the developer will become Asia’s biggest junk dollar-bond default in principal amounts since 2000, according to HSBC Holdings Plc. It’s a big ticking time bomb.

Stare at Excel spreadsheets all you want: the money anyone thought there just isn’t. As of the end of January, China Fortune Land held 23.6 billion yuan ($3.65 billion) in cash, of which 22.8 billion was in restricted funds collected mainly from property pre-sales, according to a Feb. 2 filing. And the company is already 5.3 billion yuan overdue on bank loan repayments.

The math came as a shock to stockholders. The last time the public heard about China Fortune Land’s cash position was late October, when it posted third-quarter results. Back then, the company held 38.6 billion yuan in cash, almost all of which was unrestricted. So where did the billions go? What was the developer’s monthly cash burn rate? Where were the numbers that would have told analysts this was likely to happen?

There’s so much information dislocation that some people are willing to pay tens of thousands of dollars for it. Debtwire and REDD Intelligence cost upwards of $10,000 per year. That pricey information, of course, is not available to an average investor.

There’s now a tug of war between the developer and the debt news services. On Feb. 3, REDD Intelligence and Debtwire both reported that company management had told investors it would suspend all debt repayments, thereby sending its bonds to record lows. One day later, the developer denied it. Investors need to be “rational” and follow official announcements only, the company said in a filing.

If investors did just that, they would have not a penny left. In China, public filings are infrequent. In addition, well-connected brokerages arrange exclusive conference calls for their clients to engage with the company – and sometimes, market-moving information from these meetings leak out to reporters. Case in point: Before it held its first credit committee meeting on Feb. 1, China Fortune Land’s bond due Feb. 28 was already trading at 57 cents on the dollar on the news. Professional investors know the subscription is worth it.

At this point, with so little cash on hand, China Fortune Land will almost certainly have to restructure its debt load to avoid a default. It’s even more crucial that the company updates its financials regularly – and to a broader investor base. Not knowing much – or perhaps knowing too much – mainland investors are aggressively paring down their bond positions to trade at as low as 3.5% of face value. That can’t be good for refinancing.

China Fortune Land did not respond to Bloomberg Opinion queries about why it did not update investors on its diminished cash positions faster, or whether it plans to host public briefings regularly to address its debt situation.

Meanwhile, speculation is rampant. Will China Fortune Land find a white knight in the shape of its second largest shareholder — Ping An Insurance Group Co. of China, which may otherwise have to write down its 54 billion yuan exposure? Will the Hebei government come to the rescue? The company’s bond prices oscillate with each new guess.

The situation in the U.S. is different — and American investors should feel fortunate. Take AMC for example. The movie theater chain is so much more transparent — even though its majority stockholder is Dalian Wanda Group, a Chinese company. Just like China Fortune Land, AMC has a liquidity issue. With most of its cinemas closed amid Covid, it was running out of money. But through the many detailed filings required by the Securities and Exchange Commission, potential investors can estimate that it has raised enough cash to last about a year — even if the Covid-19 situation does not improve. And just like that, AMC’s distressed bonds became a bargain.

Investing in distressed companies in China is more art than science, a polite analyst might say. But, really, it’s more a playground for rampant speculations and financial conspiracy theories. You might be able to crunch the cash flow numbers better than anyone else, but that does not mean you will emerge a winner in China.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Shuli Ren at sren38@bloomberg.net

No comments:

Post a Comment