Champion of Key Fed Inflation Gauge Says Policy Shift Is Needed

- 5-year, 5-year forward rate is now consistent with Fed goal

- Former Fed official Sack says further climb would be problem

The economist who helped change the way the Federal Reserve assesses long-run inflation expectations says their current level means the central bank needs to start laying the groundwork for shrinking its massive bond-buying program.

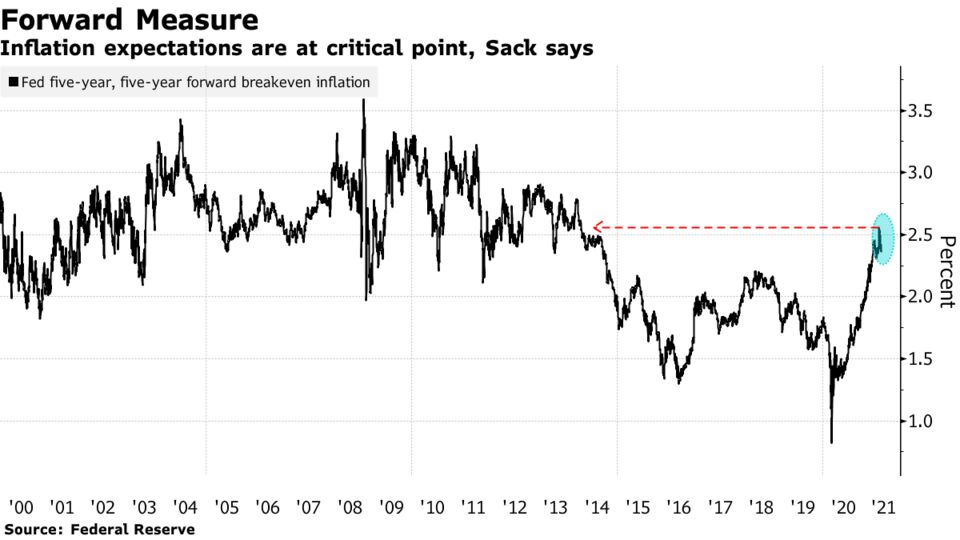

As head of monetary and financial market analysis at the Fed Board of Governors almost two decades ago, Brian Sack and his colleagues championed the use of a forward measure of inflation expectations to help guide policy. Now director of global economics at hedge fund D.E. Shaw & Co., he says the so-called five-year, five-year forward breakeven inflation rate has climbed to a level where further increases would be problematic for the central bank.

The rate, which looks past some of the short-term noise that affects consumer prices, reached a seven-year high last month of 2.55%. That level translates into an average of over 2% annually during the half decade beginning in 2026 on the price measure the Fed actually targets. So the central bank is effectively on course to achieve its average 2% inflation goal in the eyes of investors.

The rebound from ultra-depressed levels seen during the pandemic’s initial onslaught is beneficial, Sack says. But advancing much further risks pushing inflation expectations to levels that would make it harder for the Fed to meet its twin objectives of stable prices and maximum employment.

“Inflation expectations have already risen to a level consistent with the Fed’s mandate, so my view is that the Fed should not allow them to rise further,” said Sack, who also formerly headed the New York Fed’s markets group. “It may be time to adjust the policy message to reflect that.”

The tweak in signaling may already have begun. An array of Fed officials have indicated that it may be getting close to the time to debate trimming the bond purchases. The Fed is currently adding $80 billion of Treasuries and about $40 billion in mortgage-backed securities every month to its balance sheet, to support growth and keep markets functioning smoothly. Officials aren’t expected to adjust that pace at their meeting next week.

Crucial Debate

Most Fed officials insist that inflationary pressures bubbling up now are mainly the transitory result of imbalances between supply and demand as the economy revives. Recent readings are also unusually elevated when compared to the extraordinarily low levels registered a year ago.

Treasury Secretary Janet Yellen told Bloomberg News on Sunday that President Joe Biden should push forward with his $4 trillion spending plans even if they fuel inflation that persists into next year and higher interest rates. But she said the packages wouldn’t be enough to cause an inflation over-shoot.

Economists such as Roger Bootle, Jason Furman and Lawrence Summers are less confident that that the acceleration in inflation will prove temporary. Summers, for example, has warned that besides pressure from stimulus and pent-up demand, rising costs for housing, medical services and labor will also come into play.

It’s a crucial debate for central bankers, who view expectations for price pressures as a big part of the actual trajectory of inflation. The dynamic has become even more important in the wake of their new approach to targeting inflation: To help the economy recoup lost jobs, the Fed now plans to keep rates low until price gains average 2% over time, contingent on longer-term inflation expectations also remaining well anchored at that level.

The five-year, five-year forward breakeven inflation rate measures bond traders’ projection for average annual consumer price increases for the five years beginning in 2026. It’s derived from the most widely known market yardstick for inflation expectations: the outright breakeven rate, which measures the gap between yields on Treasury Inflation-Protected Securities, or TIPS, and standard Treasuries. The idea is to create a smoother read on this policy ingredient, one that filters out the noise of the coming few years.

Market Signal

The 10-year breakeven rate touched 2.59% on May 12, its highest since 2013, after surging from a nadir of 0.47% in March 2020. It traded around 2.4% Tuesday.

Some investors have downplayed the climb in breakevens, saying they need to be adjusted lower because the readings also reflect the premium resulting from inflation risk -- which they contend is more about uncertainty over the path of price pressures than actual inflation expectations.

Sack doesn’t agree. His analysis shows that inflation risk premium is actually negative, or at most zero, which would mean actual inflation expectations are higher than breakevens indicate. That’s because when the economy sours, prices of risky assets tend to decline and so do breakevens. The poor liquidity of TIPS trading during such stretches is also a factor.

The Fed, of course, looks at an array of measures to estimate inflation expectations, including surveys. It publishes a composite index of common inflation expectations that uses 21 inflation indicators -- including the five-year, five-year forward rate.

U.S. consumer prices climbed in April by the most since 2008, rising 4.2% from the same period a year earlier. The reading for May, to be released Thursday, is forecast to show prices accelerated at a 4.7% annual clip.

Kicking off tapering discussions would mark a big moment for financial markets as it would be a precursor to a pull-back in the Fed’s support for the economy.

With the nation’s vaccine roll-out sparking a surge in consumer spending, forecasts for growth are mounting accordingly. Economists predict a roughly 9% annualized pace of expansion this quarter, after a 6.4% rate last quarter.

“Doing QE in a quarter when the economy is growing so rapidly isn’t going to help contain inflation expectations,” Sack said.

No comments:

Post a Comment