Hello, this is Jill Disis in Hong Kong.

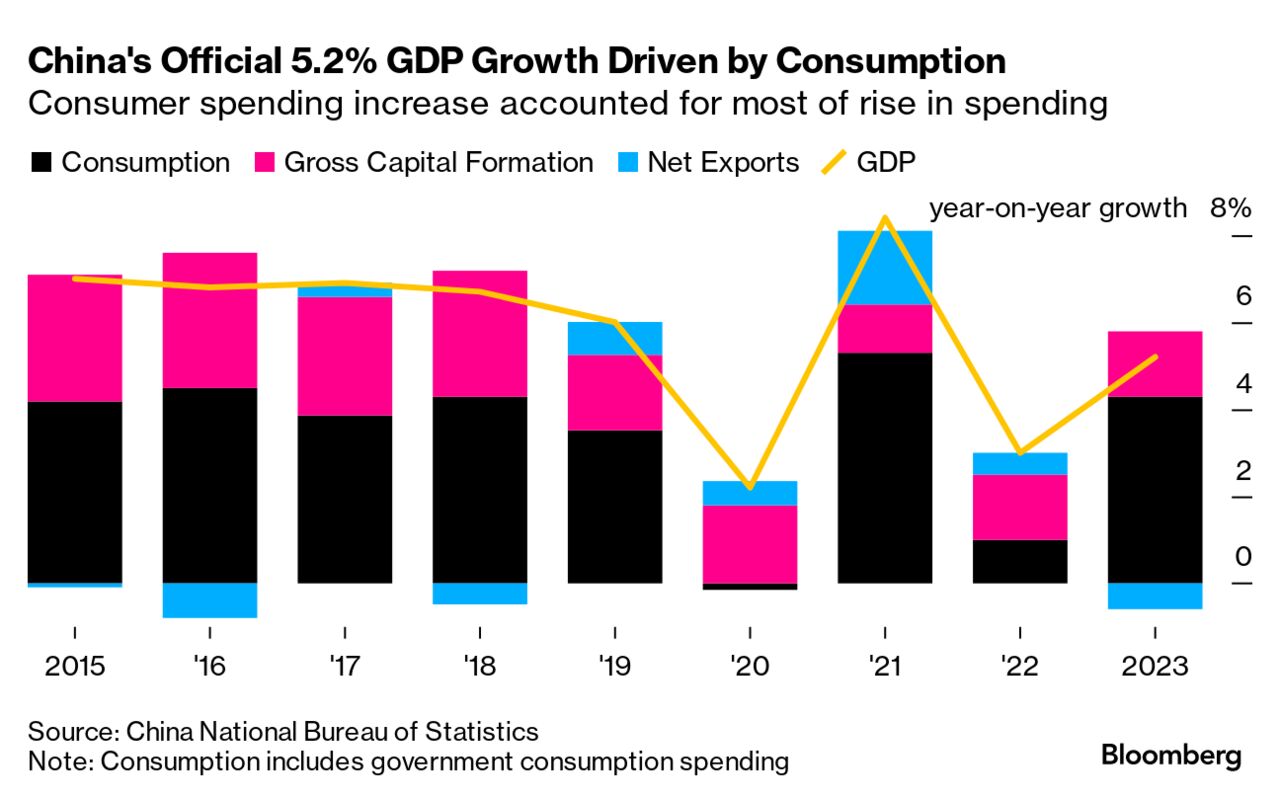

China seemingly notched a win for its economic goals this week when it reported that GDP growth last year hit 5.2% — bang on its official target of “around 5%” set last March.

Authorities were so confident that Premier Li Qiang revealed the number during a speech to the world’s elite in Davos, Switzerland, a day before China’s statistics department did. It’s the first time I have seen that kind of front-running for such a critical piece of economic data.  So why are investors — and economists — so dour?

While that headline figure looks passable, you don’t have to dig too deeply to see where the trouble spots are for the world’s second-largest economy.

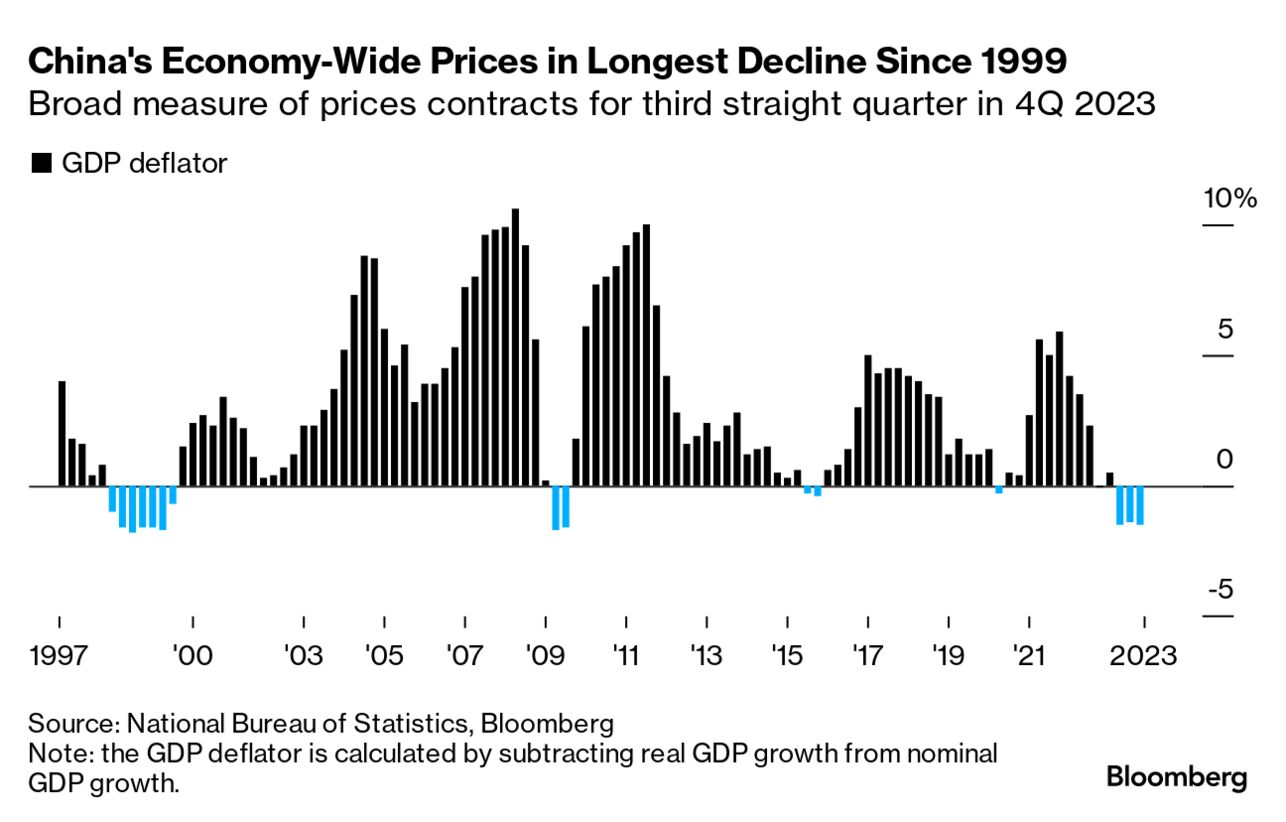

China has recorded its worst deflationary streak since the Asian Financial Crisis, with a measure of economy-wide prices falling for a third straight quarter to close out 2023.

The rout in the property sector also shows no signs of letting up, with real estate investment and housing new starts both plunging last year. Manufacturing for EVs and solar panels is booming, but those sectors are nowhere near big enough to replace housing as a growth driver.

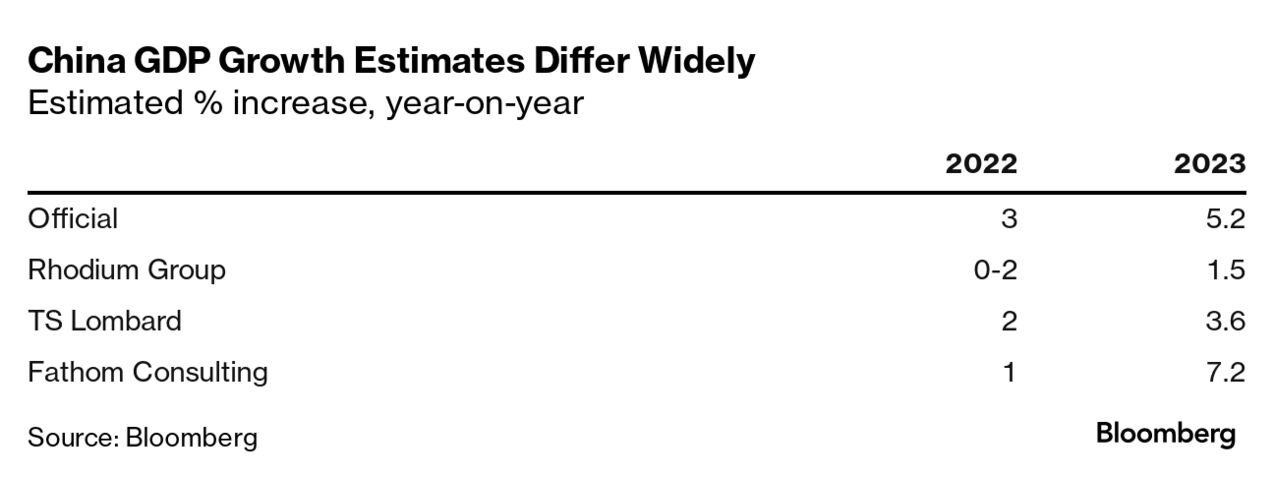

Even the GDP figure is a subject for debate, given longstanding suspicions about the accuracy of those numbers. The research provider Rhodium Group thinks growth last year was likely around 1.5%.  All those concerns are leading economists and investors to focus on how much stimulus China will deploy this year as it works on a longer-term transition for economic development.

The thing is, many signs are pointing to a pretty cautious approach by Beijing.

“In promoting economic development, we did not resort to massive stimulus,” Li said in Switzerland as he praised last year’s rebound. “We did not seek short-term growth while accumulating long-term risk.”

China has a lot of reasons not to throw hundreds of billions of dollars worth of support at its economic problems.

That “bazooka-style” stimulus may have helped the country recover after the 2007-2008 global financial crisis, but it also led to overcapacity and saddled many local governments with huge financial burdens they’re still struggling with today. No wonder President Xi Jinping is still running his economy cold.  There are a few possibilities for support this year. The central bank could cut policy rates, though it held off doing so Monday as concerns about currency volatility and a still-hawkish Federal Reserve loom.

Bloomberg News has also reported that authorities are mulling the issuance of 1 trillion yuan ($139 billion) in ultra long sovereign bonds — though that wasn’t enough to cheer investors up.

“Authorities don’t want to give the impression that they are very worried about growth, and they want to try to see the economy through 2024 without significant stimulus,” said Louis Kuijs, chief economist for Asia Pacific at S&P Global Ratings.

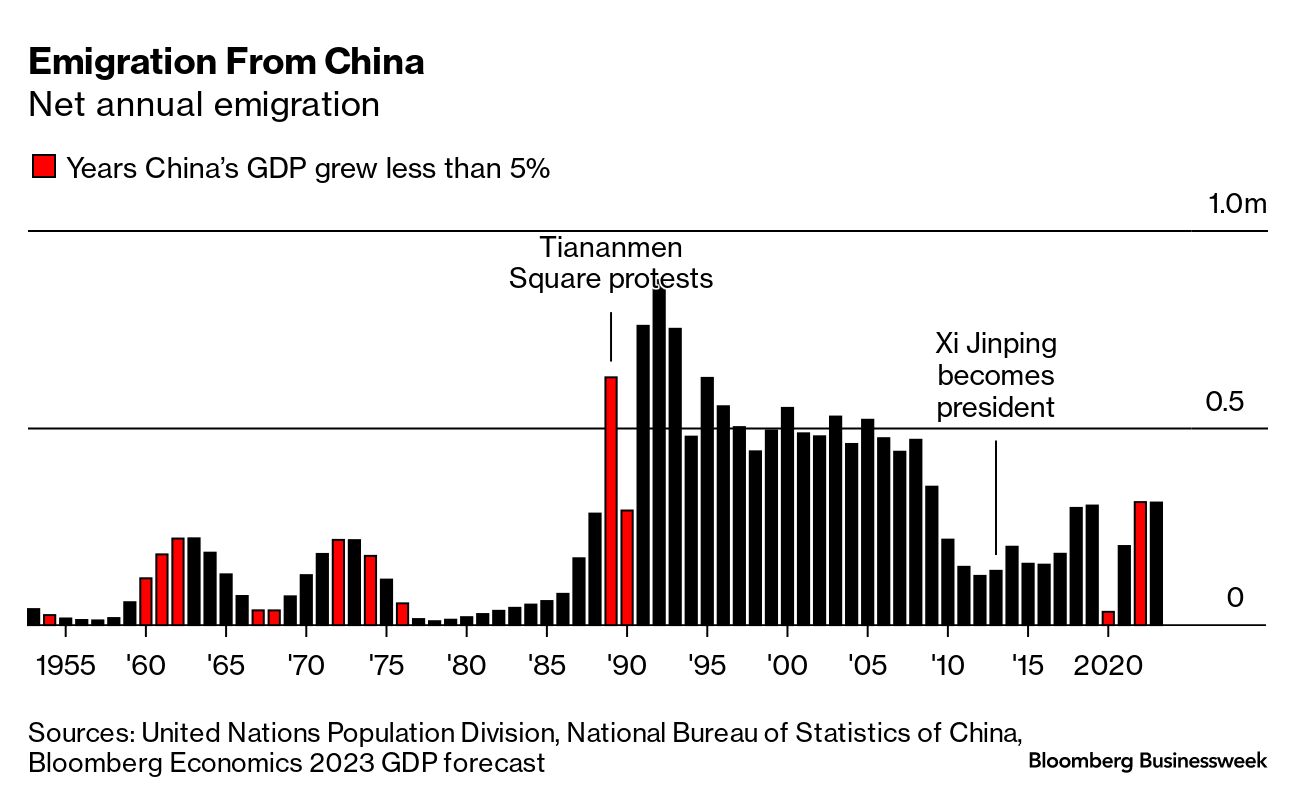

“There is a risk that they are underplaying the downward pressures on the economy.” With all the trouble and uncertainty at home, it’s only natural that some people would bolt for the door. At least 1.1 million have done just that since 2019, in search of a new life abroad. Along the way they’re changing the neighborhoods and cities they inhabit. In Bangkok, for example, a street once filled with Thai-owned stores now brims with signs in Mandarin advertising everything from pork knuckle rice to video-production services. The familiar story of gentrification is in evidence: well-to-do migrants driving up home prices and old businesses being displaced by ones catering to the new clientele.  Pracha Rat Bamphen Road in Bangkok. Photographer: Athikhom Saengchai for Bloomberg Businessweek Some of those seeking economic opportunities overseas are prepared to take extreme risks, such as illegally crossing the US-Mexico border with the help of smugglers. The route isn’t for the faint of heart. This outbound migration isn’t helping China arrest a rapid decline in its population, which fell for a second year by over 2 million in 2023. And this number doesn’t count migration. Births fell by more than 500,000 to 9.02 million last year, the lowest since the founding of the People’s Republic of China in 1949. Back then, China had just 541 million people, a little more than a third of its 1.4 billion population today. This is not a problem unique to China. Virtually all East Asian economies — Hong Kong, South Korea, Japan, Taiwan and even North Korea — are grappling with a drop in birth rates. For Beijing, a rapidly aging society would bring further headwinds to its flagging economy, in part by hurting long-term demand for housing. With fewer workers to support the growing retired population, the government may also struggle to pay for its underfunded national pension system. AI, automation and other technology may improve productivity and make up for some lost growth. Otherwise, spare a thought for young Chinese who just want to “lie flat.” |

No comments:

Post a Comment