A Bullish Alibaba Will Depend on Ant's Bottom Line

As its core business slows, the online retailer’s quarterly earnings are tied to its fintech affiliate, which is preparing an IPO.

Ant Group’s imminent initial public offering promises to make a lot of people rich, including founder Jack Ma and existing shareholders of Alibaba Group Holding Ltd.

Yet the real benefit to Alibaba is not in the value of its affiliate’s stock, which could fetch a valuation of $200 billion upon listing in Hong Kong and Shanghai, but in the ongoing earnings the financial services company will keep feeding the e-commerce giant.

Since September last year, Alibaba has recognized Ant through the equity method of accounting. That means it takes one-third of every dollar (yuan) of net income Ant earns, representing Alibaba’s 33% ownership, but won’t account for its fluctuating share price in its income statements.

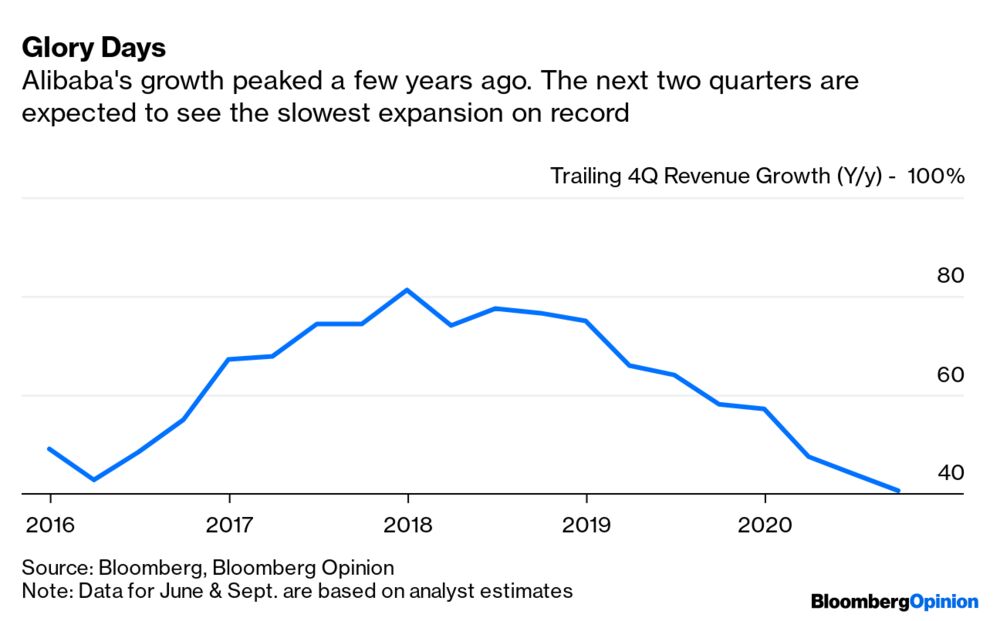

Alibaba needs that profit share.

China’s dominant online retailer is suffering its slowest growth ever, and operating margins have fallen to a third of where they were six years ago as it spends more on marketing to juice growth in a maturing economy. While profits are still decent, they’re no longer as fat or expanding as quickly as they once were. As I’ve written before, Alibaba’s heady growth days are over, and this was happening well before Covid-19 hit revenue in the March quarter.

An early post-pandemic belief that Alibaba would benefit from social-distancing and a rebound in online spending has given way to the realization that China’s domestic consumer economy isn’t immune to the global malaise. While most of the country has returned to a level of normalcy, a sharp drop in exports as the rest of the world continues to suffer makes it unlikely that even Chinese shoppers will have the confidence or ability to spend like they used to.

Ant, on the other hand, should have plenty of growth ahead. As my colleague Nisha Gopalan wrote, the timing of Ant’s IPO can be at least partly attributed to its broadened base of financial products, making it more of a platform and less of a risk to China’s financial system.

Alibaba recognized 5.3 billion yuan ($752 million) in earnings from its stake in Ant last year. But the figure understates the size of the contribution. It took the equity stake Sept. 23, so the number actually represents profit from the following day through Dec. 31. Alibaba accounts for its Ant profits one quarter in arrears, so it was seen on the books in the March period this year, which was handy because operating profit was a mere 7.1 billion yuan, down 17%, due to Covid-19.

More importantly, Ant is growing. Insurance premiums, one of many financial products it offers, doubled during the fiscal year to March 31. It has facilitated more than 4 trillion yuan in assets under management, and has 1.3 billion active annual users for its payment platforms.

As China’s domestic consumption picture loses its luster, there’s still a belief that the financial services business — including digital payments, loans, wealth management and insurance — will continue to expand. Ant’s Yu’E Bao money-market fund, for example, grew to become the world’s largest, while the nation’s insurance industry could swell to 4.9 trillion yuan by next year.

While Ant shareholders will be buying into that story, Alibaba’s bottom line is riding on it.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

No comments:

Post a Comment